The UK CBAM Arrives in 2027: How It Differs from the EU's

The UK CBAM Arrives in 2027: How It Differs from the EU's

For importers who trade across both sides of the Channel, "CBAM" is about to stop being a single rulebook. The EU's Carbon Border Adjustment Mechanism has been live since January 2026. From 1 January 2027, the United Kingdom launches its own version - similar in intent, but different in several details that matter for compliance and cost.

Here is how the two regimes line up, and what businesses caught by both should be doing now.

Same idea, one-year gap

Both mechanisms exist to put a carbon price on imports of emissions-intensive goods, closing the gap with domestic carbon pricing and discouraging carbon leakage. The EU scheme is already in its definitive, paying phase. The UK CBAM is set to go live on 1 January 2027, creating roughly a one-year offset between the two systems.

That gap matters: an importer can face a live EU obligation in 2026 and a brand-new UK obligation layered on top in 2027.

Different scope - electricity is the headline omission

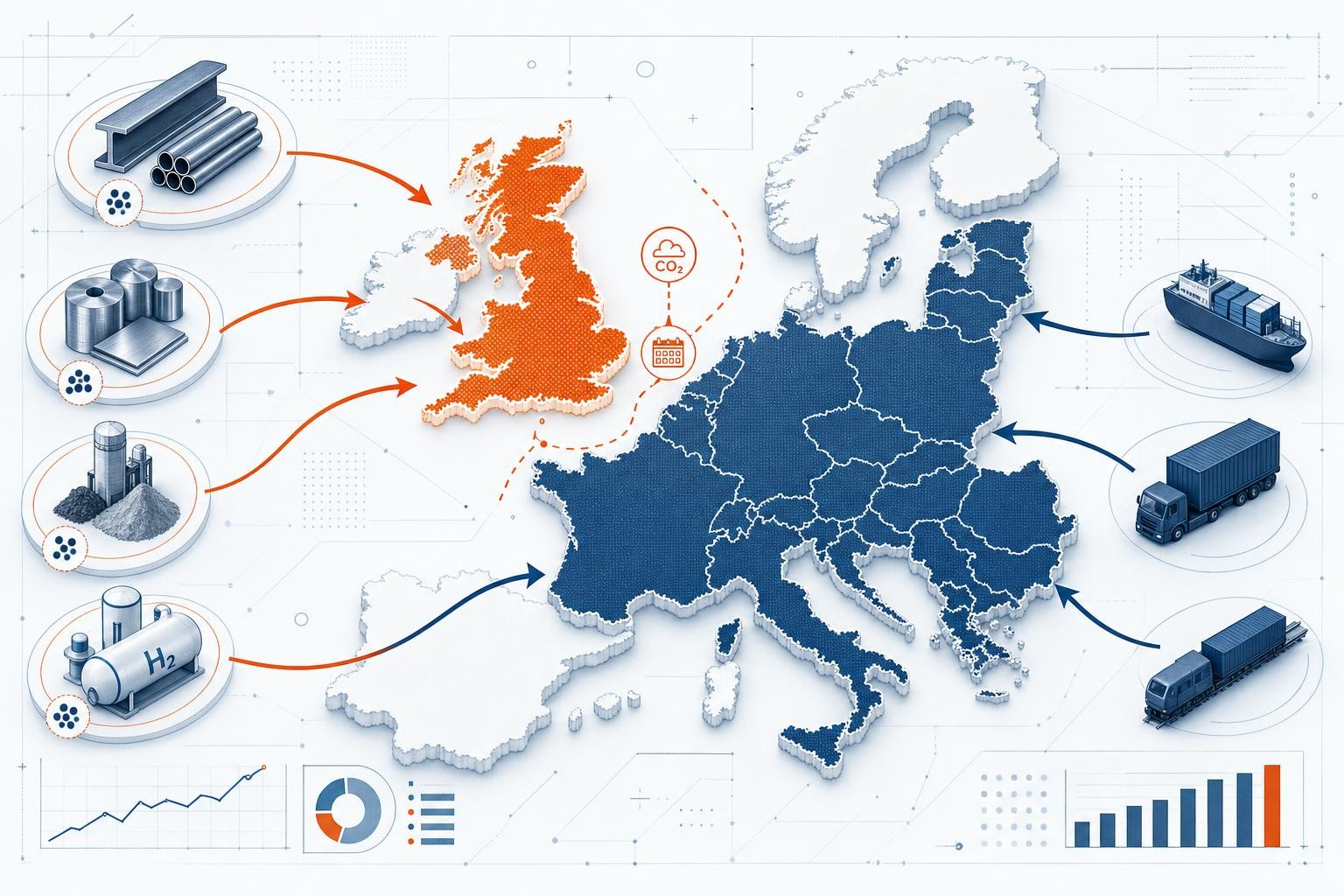

The UK CBAM will cover the aluminium, cement, fertiliser, hydrogen, and iron and steel sectors. The most significant difference from the EU scheme is that electricity is not in scope of the UK CBAM. Glass and ceramics, which had appeared in earlier UK proposals, have also been dropped for the 2027 launch.

So the UK starts with five sectors to the EU's six, and a narrower set than some had expected.

A different threshold

The EU uses a single 50-tonne mass-based de minimis threshold. The UK takes a value-based approach instead: only businesses importing £50,000 or more of CBAM goods over a rolling 12-month period will need to comply. Below that, you are out of scope. This is a meaningfully different test - a low-tonnage but high-value shipment could be caught in the UK while a high-tonnage, lower-value flow is treated differently in the EU.

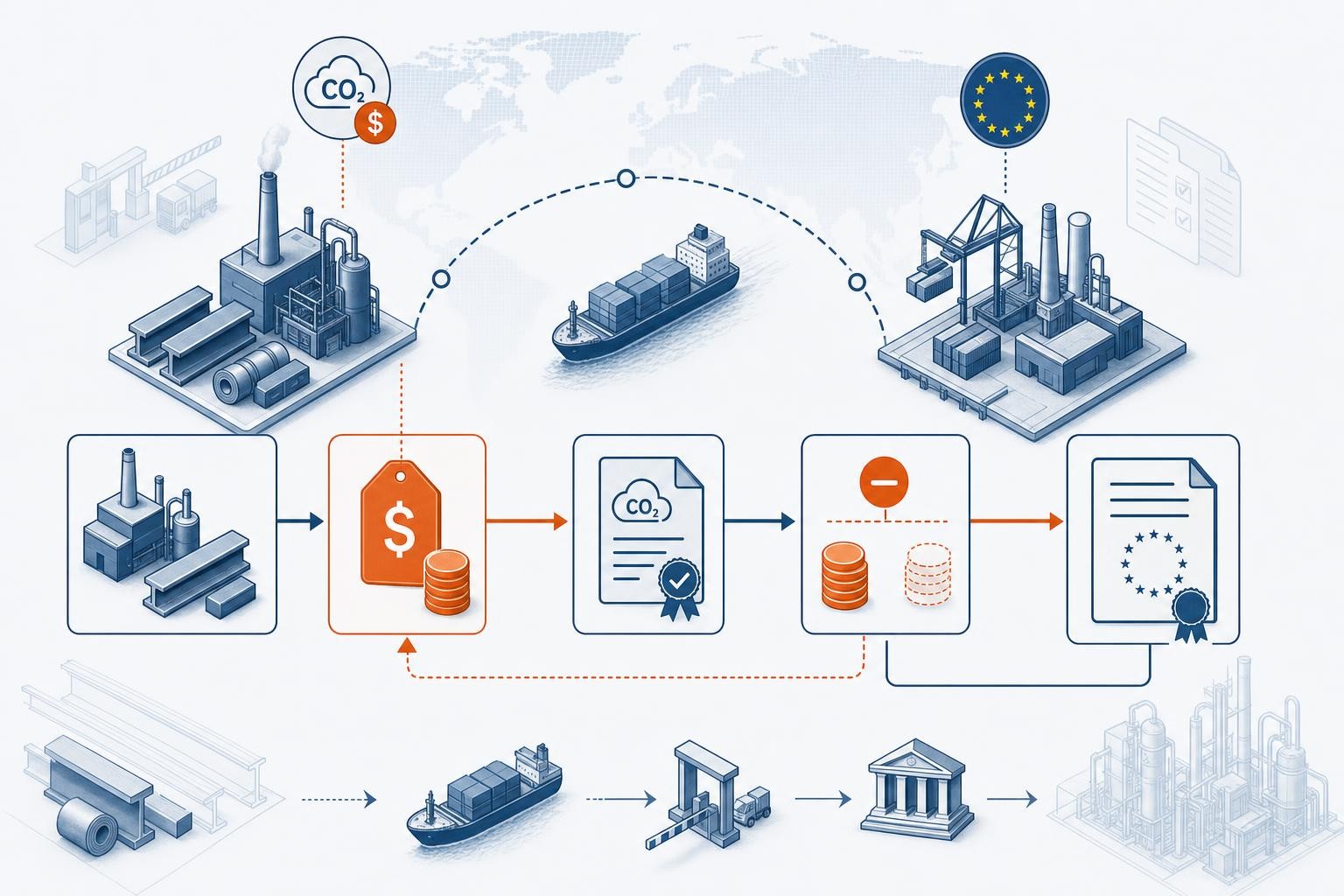

No certificates - a levy, not a market

This is the deepest structural difference. The EU model requires importers to buy and surrender CBAM certificates priced at the prevailing ETS market rate. The UK has deliberately chosen not to follow that model, judging that certificate trading would add complexity for both importers and government.

Instead, the UK CBAM works as a tax-style liability calculated on embedded emissions at a set CBAM rate, declared and paid to HMRC. The liable person is the one responsible for the goods when they are released into free circulation (or, where there are no customs controls, the person on whose behalf the goods are moved). That person registers, files returns, and pays.

Default values: one global figure

The two schemes also diverge on default values. Where the EU publishes country-and-product specific defaults with mark-ups, the UK plans to use a single default value per product, based on a global average weighted by production volumes in the UK's key trading partners. Simpler to administer - but it can produce very different numbers from the EU equivalent for the same goods.

Encouragingly, the UK's methodologies for monitoring and verifying actual emissions are designed to be broadly interoperable with the EU CBAM, which should reduce duplicated effort for suppliers reporting into both systems.

What dual-market importers should do now

- Map your exposure to both regimes. Identify which of your products and flows hit the EU's tonnage test, the UK's £50,000 value test, or both.

- Watch the sector lines. If you import electricity, you have an EU obligation with no UK equivalent; if you import the five shared sectors, plan for both.

- Reuse your supplier data. Because UK MRV is built for interoperability, verified actual-emissions data you collect for the EU should largely serve the UK too - one data-gathering effort, two filings.

- Assign the UK liable person early. Clarify now who in your import chain will register with HMRC and file UK CBAM returns from 2027.

The destination is the same - a carbon price at the border - but the routes differ enough that "we already do EU CBAM" is not a complete answer for the UK. Treat 2027 as a distinct compliance project that happens to share data with the one you are already running.

This guide is general information, not legal or tax advice. UK CBAM detail is still being finalised in legislation; confirm against the latest HMRC and European Commission guidance.

Related reading

CBAM and Hydrogen: A Plain-English Guide for Importers

Hydrogen is one of CBAM's six covered sectors - and one of only two with no 50-tonne exemption. Here's what that means for importers, how embedded emissions are counted, and what to do first.

How to Deduct a Carbon Price Already Paid Abroad from Your CBAM Bill

The EU's June 2026 draft implementing rules finally explain how importers can offset a carbon price paid in a supplier's country against their CBAM certificate obligation. Here's what the rules say.

CBAM Penalties Explained: What EU Importers Risk in the Definitive Period

The CBAM definitive period is live. Miss the surrender deadline or breach the quarterly holding rule and you face €100/tonne - plus you still owe the certificates. Here's exactly how it works.