CBAM and Hydrogen: A Plain-English Guide for Importers

CBAM and Hydrogen: A Plain-English Guide for Importers

Hydrogen rarely tops the list when people think about the EU's Carbon Border Adjustment Mechanism (CBAM). Steel, aluminium and cement get the headlines. But hydrogen is one of the six original sectors CBAM covers, and it carries a quirk that catches importers off guard: it is one of only two product groups with no minimum-volume exemption at all.

If you bring hydrogen into the EU, this guide explains what is in scope, how your emissions are counted, when the costs land, and what to do first.

Hydrogen is squarely in scope

Hydrogen sits alongside cement, iron and steel, aluminium, fertilisers, and electricity as one of the goods CBAM was designed to cover from the outset. These sectors were chosen because they are carbon-intensive and at the highest risk of "carbon leakage" - the shifting of production outside the EU to avoid carbon costs.

CBAM has been in its definitive period since 1 January 2026, the point at which the mechanism moved from simple reporting to real financial obligations. From that date, importers must declare the emissions embedded in their goods and, in time, pay for them.

The catch: no 50-tonne exemption for hydrogen

The 2025 Omnibus simplification introduced a single, mass-based de minimis threshold: importers bringing in 50 tonnes or less of CBAM goods per year are exempt. For steel or aluminium importers, that change took a large number of small players out of scope entirely.

Hydrogen does not get that relief. Hydrogen and electricity are explicitly excluded from the 50-tonne exemption. In practical terms, any quantity of imported hydrogen can trigger CBAM obligations. If hydrogen is part of your import portfolio, you cannot assume you are too small to be caught.

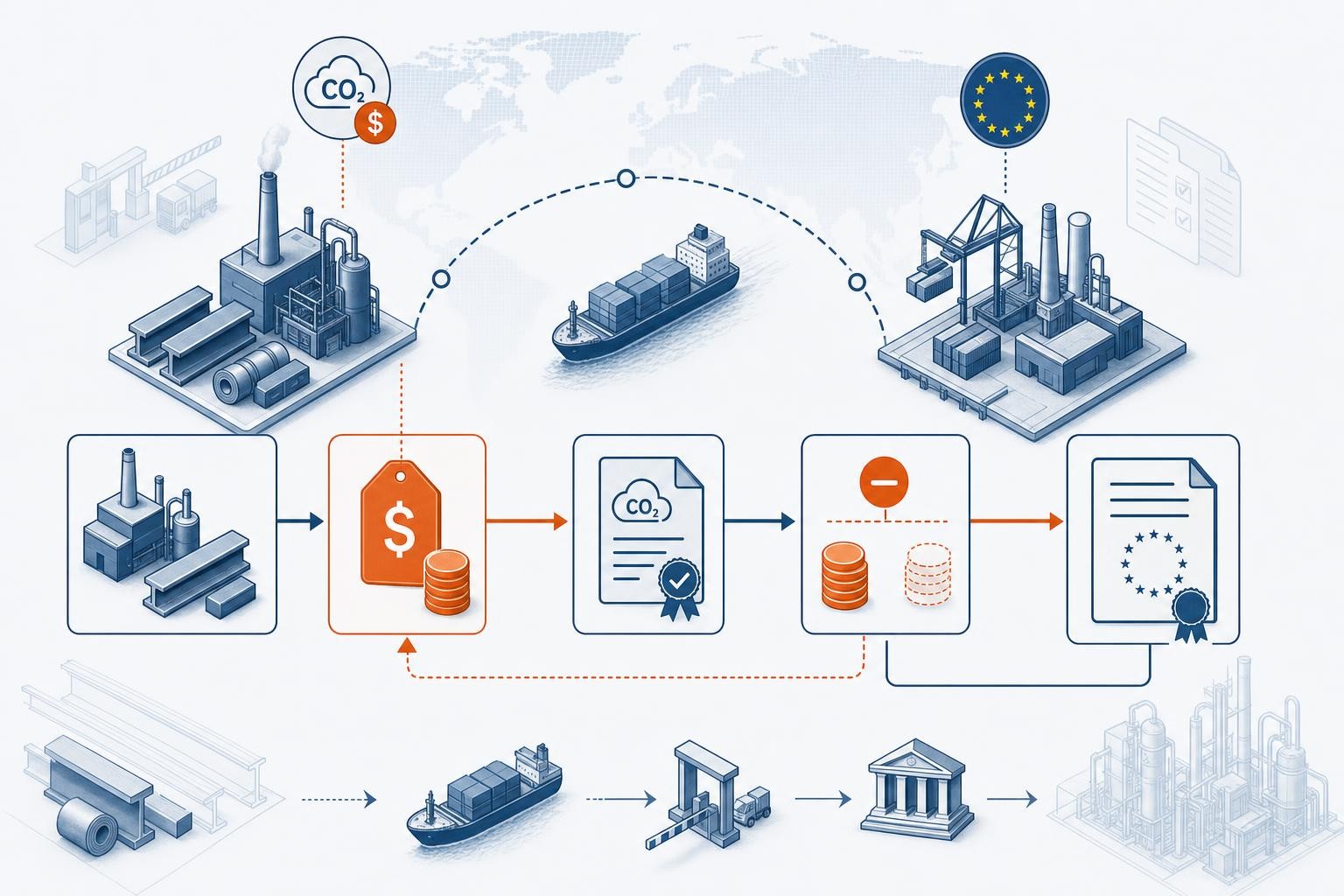

How embedded emissions are counted

CBAM charges you for the greenhouse gases embedded in the production of what you import - not just the gas itself but the emissions released making it. For hydrogen, the production route matters enormously: grey hydrogen made from unabated natural gas carries a very different footprint from low-carbon hydrogen.

You have two ways to determine those embedded emissions:

- Actual values drawn from your supplier's installation, calculated to EU rules and capable of being verified by an accredited third party.

- Default values, which are country-and-product average intensities published by the Commission, applied with a deliberate mark-up.

Because the default values include a conservative mark-up, relying on them generally means surrendering more certificates than if you used solid supplier data. For a high-variance product like hydrogen, the gap between a clean actual figure and a defaulted one can be substantial.

When the money actually moves

The financial mechanics are staggered. Although the definitive period began in January 2026, the sale of CBAM certificates was postponed to 1 February 2027. Declarants buy certificates in 2027 to cover the embedded emissions of their 2026 imports.

Certificate prices track the carbon market: the price for the 2026 compliance year reflects the quarterly average of 2026 EU ETS allowance prices. Your first annual CBAM declaration covering 2026 imports is due by 30 September 2027.

What hydrogen importers should do first

- Confirm your status. Because there is no volume exemption, treat every hydrogen import as in scope and make sure you are (or are becoming) an authorised CBAM declarant.

- Map your production routes. Identify, supplier by supplier, how the hydrogen you buy is made. This drives both your emissions figure and your certificate cost.

- Start the data conversation now. Ask suppliers for installation-level, verifiable emissions data rather than defaulting. The mark-up on default values is a real, recurring cost.

- Model the 2026 liability. Even though you pay in 2027, the exposure is building today. Estimate it now so it is not a surprise.

Hydrogen's role in EU industrial decarbonisation will only grow, and so will scrutiny of its supply chain emissions. Getting your CBAM processes right for hydrogen early - especially the supplier-data piece - is the difference between a manageable cost and an avoidable one.

This guide is general information, not legal or tax advice. Confirm specifics against the latest European Commission CBAM guidance and your own customs position.

Related reading

How to Deduct a Carbon Price Already Paid Abroad from Your CBAM Bill

The EU's June 2026 draft implementing rules finally explain how importers can offset a carbon price paid in a supplier's country against their CBAM certificate obligation. Here's what the rules say.

CBAM Penalties Explained: What EU Importers Risk in the Definitive Period

The CBAM definitive period is live. Miss the surrender deadline or breach the quarterly holding rule and you face €100/tonne - plus you still owe the certificates. Here's exactly how it works.

CBAM and Cement: A Plain-English Guide for EU Importers

Cement and clinker are in CBAM's definitive phase from 1 Jan 2026. This plain-English guide covers CN codes, why process emissions make cement uniquely exposed, default-value penalties, and what to do first.