How to Deduct a Carbon Price Already Paid Abroad from Your CBAM Bill

If your steel supplier in South Korea or your aluminium smelter in the UK already pays a carbon price on the tonnes of CO₂ embedded in the goods they ship to you, the EU does not intend to charge you again for the same emissions. That principle has been in the CBAM Regulation since day one - but the detailed mechanics of how to claim the deduction have been missing. That gap closed on 13 May 2026, when the European Commission published a draft implementing regulation on carbon prices paid in third countries, open for public consultation until 10 June 2026.

This post unpacks what the draft says, what it still leaves open, and what you should be doing now. Note throughout: these are draft rules, subject to change before formal adoption.

The core principle: no double-pricing the same tonne

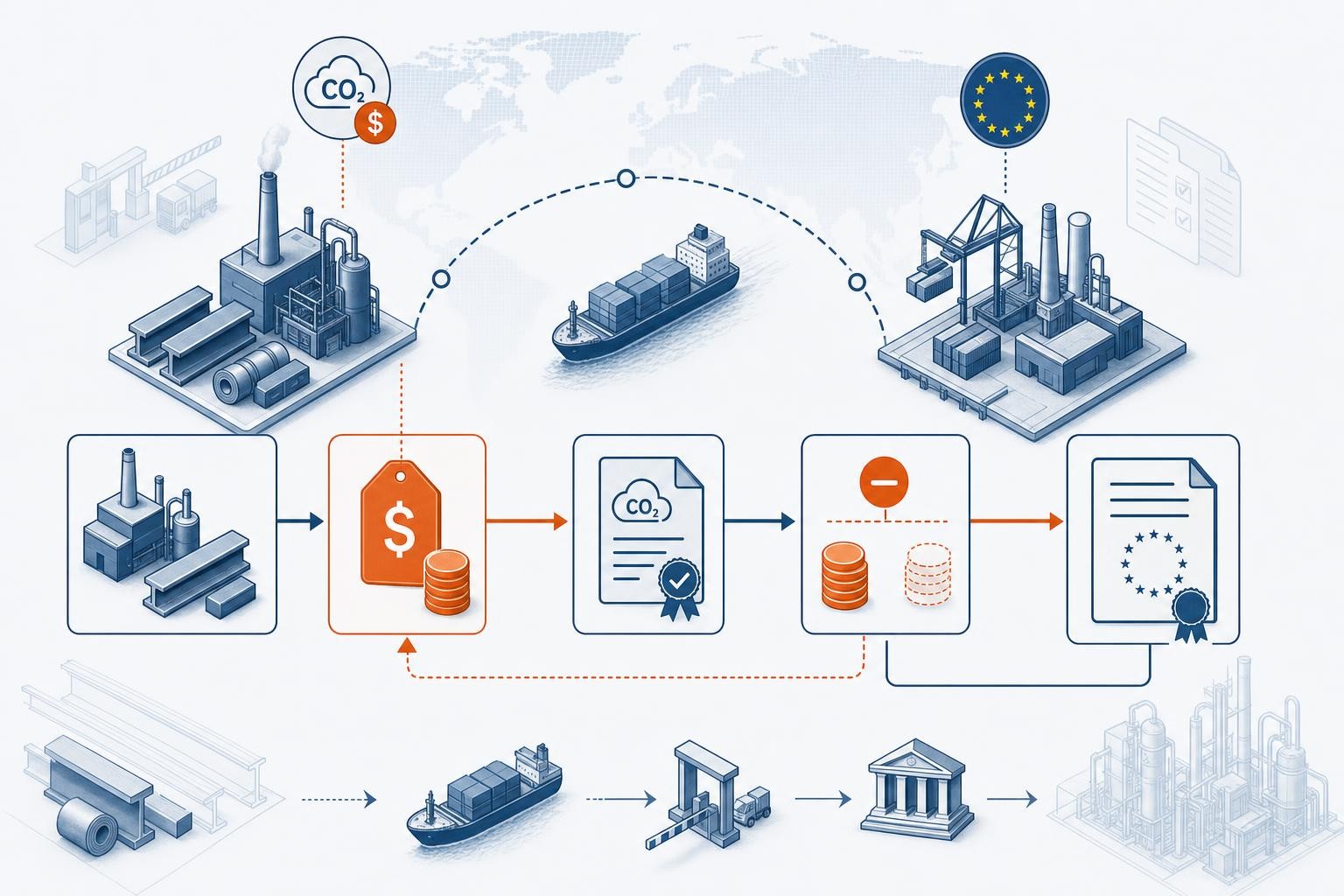

The purpose of the deduction, as stated in the draft, is to ensure that a carbon price is not paid twice on the same emissions. In practical terms: if your supplier's installation is covered by a binding carbon pricing mechanism - an ETS or a carbon tax - and that price was effectively paid during production, you as the authorised CBAM declarant can claim a corresponding reduction in the number of CBAM certificates you must surrender.

The reduction is not a rebate of cash. It is a reduction in certificate volume. Fewer certificates surrendered means a lower CBAM bill.

What the June 2026 draft adds

1. A conversion methodology

Previously, importers had no official formula for translating a foreign carbon cost into a certificate reduction. The draft fixes that. It prescribes a formula that converts the effective carbon price paid into an equivalent number of CBAM certificates, benchmarked against the yearly CBAM certificate reference price. Currency conversion uses yearly average euro exchange rates to be published by the Commission - so the maths is standardised, not left to each importer to improvise.

2. Four qualifying mechanism types

Rather than naming individual national schemes, the draft sets out broad eligibility criteria. Four types of foreign carbon price mechanism now have a recognition pathway:

The four qualifying mechanism types under the draft are: emissions trading systems (ETSs), point-source carbon taxes, fuel-based carbon taxes, and mixed-compliance systems.

The critical requirement in each case is that the mechanism must be legally binding and mandatory - it must impose compliance obligations on covered installations. Voluntary offset schemes, corporate net-zero pledges, and non-binding carbon pricing initiatives do not qualify. If your supplier's country has a carbon pricing programme that participation is optional, it counts for nothing under CBAM.

3. Independently verified evidence - mandatory

This is the part that will drive the most operational work. To claim a reduction, third-country operators must prepare a carbon price report using a standard electronic template in English, setting out the calculation steps and supporting evidence. That report must then be certified by an independent person.

What counts as evidence will depend on the mechanism type. It may include auction price data, registry records of surrendered allowances, tax authority documentation, or records of carbon credit purchases. The accredited verifier may also need to conduct site visits.

The requirements for those independent certifiers are strict:

- They must comply with international standards for conformity assessment.

- They must demonstrate technical competence in carbon pricing and emissions accounting.

- They must be accredited specifically for the certification of carbon price reports.

Accreditation is valid for five years and subject to annual surveillance. Verifiers can be established in any third country, but they must be accredited by EU accreditation bodies - the same framework that governs CBAM emissions verifiers generally.

Your supplier — not you — prepares the carbon price report and gets it certified. But you need that certified report to claim the deduction in your CBAM declaration. Start the conversation with your suppliers now, before verification backlogs build up in 2027.

The multi-jurisdictional production nuance

Most importers assume the deductible carbon price must come from the country where the finished good was made. The draft goes further. Carbon prices paid in a third country other than the country of origin of the imported goods are also eligible for deduction, provided corresponding evidence can be supplied. This matters for complex supply chains - for example, a steel precursor priced under an ETS in country A, exported to country B for finishing, then shipped to the EU from country B. The carbon cost incurred in country A is not automatically lost; it can still count, if it can be evidenced.

The Article 6 credit cap: 10%

Some third-country carbon pricing mechanisms allow operators to meet part of their compliance obligation using international carbon credits - credits generated by mitigation activities elsewhere. The draft permits those credits to count toward the carbon price for CBAM purposes, but with a hard ceiling.

The Commission caps the use of international Article 6 (Paris Agreement) credits at 10% of reported emissions; any usage beyond this threshold receives a zero carbon price for CBAM purposes.

The Commission's position here is notably more permissive than the European Parliament's ENVI committee, which called the inclusion of Article 6 credits "premature and counterproductive." The 10% cap may yet shift before the regulation is finalised.

Net of rebates: the amount that actually counts

The deductible amount is not simply the headline carbon price your supplier faces. It is the net amount effectively paid - after any compensation that reduces the real cost.

The draft is explicit: any rebates, free allowances, tax exemptions, refunds, or indirect cost compensation related to electricity pricing must be subtracted from the deductible amount. If a government gives back part of the carbon cost through export incentives or free allocation, that portion does not count.

There is one carve-out. Revenues that a jurisdiction recycles back into decarbonisation support for the same installations are excluded from the compensation calculation - provided the support is granted transparently, is open to all covered operators, and is explicitly targeted at emissions reduction. This mirrors how the EU treats ETS revenues reinvested in the green transition.

The practical implication: if your supplier operates in a country with generous free-allowance allocation or export rebates, the effective deductible price may be substantially lower than the nominal carbon price in that market.

Two calculation routes: default or actual

The draft offers two paths for calculating the deduction:

| Feature | Default carbon price | Actual carbon price |

|---|---|---|

| What it is | A standard annual average price published by the Commission for countries with qualifying mechanisms | The carbon price the specific installation actually paid, based on verified data |

| Evidence burden | Lower — relies on Commission-published figures | Higher — requires a certified carbon price report from an accredited verifier |

| Accuracy | May under- or over-state the real cost | Reflects the installation's actual compliance cost |

| Availability | Commission to publish default prices in the CBAM Registry from 2027 | Available now in principle, once verification infrastructure is in place |

| Best for | Suppliers in countries with transparent, well-documented carbon prices | Suppliers who paid a higher-than-average price and want full credit |

The Commission has signalled it will publish default carbon prices in the CBAM Registry, which could simplify the deduction process - particularly for precursor goods and indirect emissions. Until those defaults are published, importers relying on actual prices need the full verification chain.

Practical steps for importers

Identify which of your CBAM goods come from countries with a qualifying ETS or carbon tax. The UK, South Korea, China (ETS), Canada, and several others have binding mechanisms — but check whether your supplier's specific sector and installation type is covered.

The certified carbon price report is the supplier's responsibility to prepare, but you need it. Raise this in your supplier conversations now. Verification backlogs are likely once certificate surrender deadlines approach in 2027.

Ask your supplier whether they receive free allowances, export rebates, or tax refunds that reduce the effective carbon price. The deductible amount is the net cost after those adjustments.

If your supplier's compliance mechanism relies heavily on international carbon credits, confirm that credits account for no more than 10% of reported emissions — otherwise the excess counts as zero for CBAM purposes.

A carbon price deduction only applies when you use actual embedded emissions data (not Commission defaults). If your supplier has a meaningful carbon price to deduct, the case for investing in actual-value verification strengthens considerably.

The draft was open for feedback until 10 June 2026. The final text may differ — particularly on the Article 6 cap and the treatment of specific mechanism types. Watch the Commission's CBAM legislation page for the adopted version.

The bigger picture

Once finalised, the carbon price deduction rules will apply retrospectively to CBAM goods imported from 1 January 2026. That means the deductions you can claim in your first CBAM declaration - due by 30 September 2027 - will cover the full 2026 import year. Getting the documentation right now, rather than scrambling in mid-2027, is the difference between claiming the deduction and leaving money on the table.

The draft also represents, as one industry commentator put it, "the final piece of the CBAM puzzle" - completing the core technical framework alongside the implementing regulations on embedded emissions, verification, the registry, and certificate pricing adopted in late 2025.

This post is an independent plain-English explainer. It is not legal or compliance advice. The implementing regulation described here is a draft subject to change. Always refer to the official European Commission CBAM legislation page and seek qualified advice for your specific situation.

Related reading

CBAM Penalties Explained: What EU Importers Risk in the Definitive Period

The CBAM definitive period is live. Miss the surrender deadline or breach the quarterly holding rule and you face €100/tonne - plus you still owe the certificates. Here's exactly how it works.

CBAM and Cement: A Plain-English Guide for EU Importers

Cement and clinker are in CBAM's definitive phase from 1 Jan 2026. This plain-English guide covers CN codes, why process emissions make cement uniquely exposed, default-value penalties, and what to do first.

CBAM certificates: how buying and surrendering will work from 2027

Certificate sales start on 1 February 2027 on a central EU platform. Here's how purchasing, the 50% quarterly holding rule, and the first surrender deadline of 30 September 2027 actually work.